For many smaller financial institutions, risk and compliance has become increasingly heavy.

New obligations are added, existing frameworks are expanded, and more reports are produced. Management and governance seek more evidence and before long, small teams can feel like they are spending more time maintaining the compliance machine than understanding whether it is actually preventing harm.

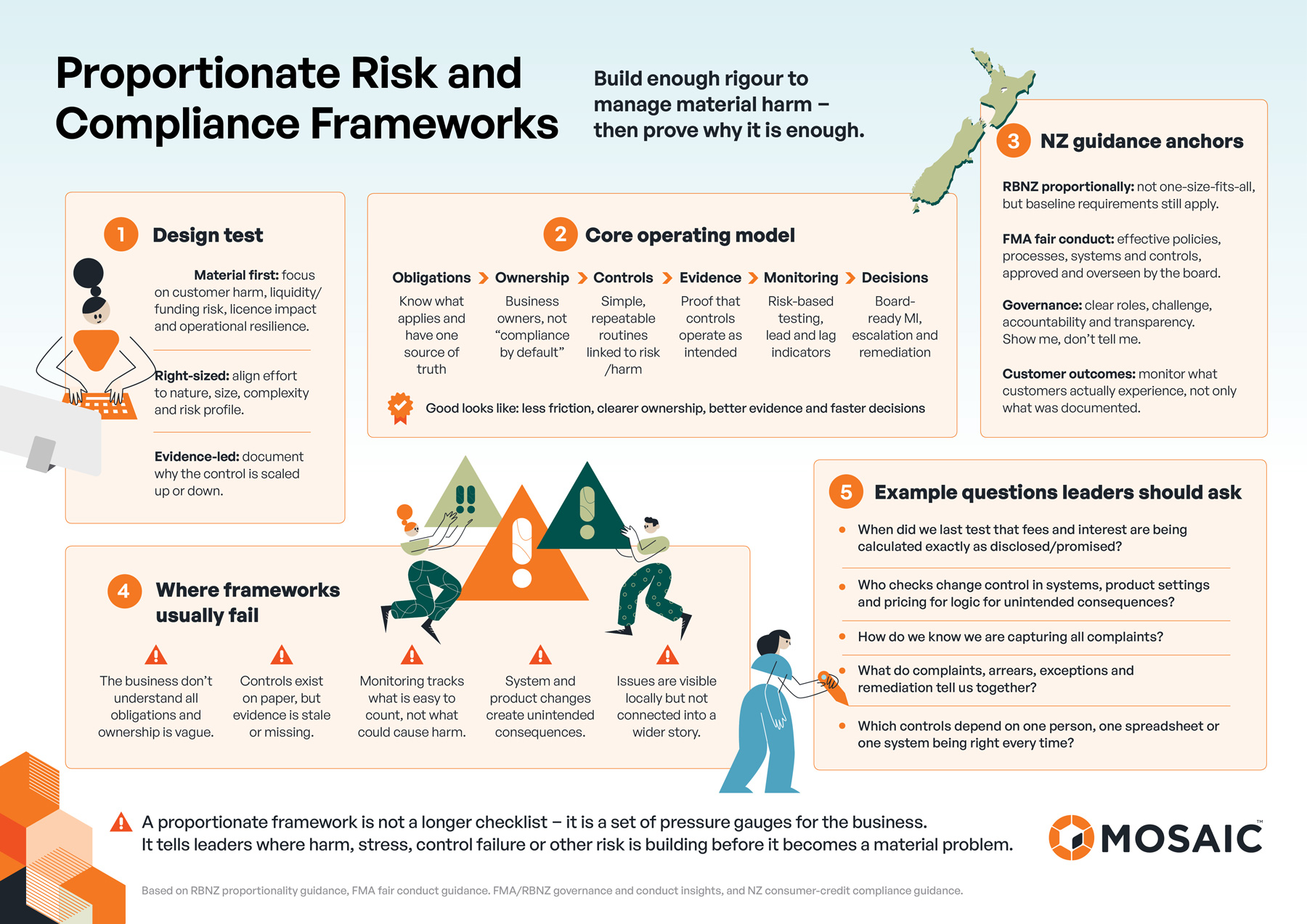

A strong risk and compliance framework should help the business see where customer harm, financial stress or control failure is building early enough to act. The goal isn’t to build the largest framework, it’s to build the right framework, with enough rigour to manage the material risks.

Proportionality is sometimes interpreted as a lighter-touch approach. It is better understood as a deliberate choice about where to apply effort. The greater the potential harm, risk or complexity, the stronger the control and assurance should be. Where the risk is lower, there should be room to simplify.

To get here though, you must first understand your obligations. Then a set of questions can ensure on establishing what right-size is for you. A proportionate approach starts with practical questions, such as ‘what harm is this obligation intended to prevent?’, ‘how material is it for our organisation?’ and ‘where are we relying on manual processes, spreadsheets or individual knowledge?’

The answers can then inform the depth of controls needed, the frequency of monitoring and the level of assurance. For example, a high potential harm activity that changes frequently (interest rates or fees for example) may require detailed controls, regular testing and periodic independent assurance. A stable, lower-risk activity may be managed through simpler evidence, periodic sampling and automated reminders.

Managing risk and compliance is sometimes seen as the job of the risk and compliance team. But in fact, the people who design products, configure systems, communicate with customers and operate processes are usually the best people to identify where the risks sit and what the controls are intended to achieve.

This is why ownership matters as much as documentation. A well written policy provides little comfort when no one owns the underlying control, no one knows what evidence should exist and no one checks whether the control worked.

The framework has to operate, otherwise what’s the point?

A practical framework should connect six things:

When these elements are connected, the framework becomes part of the operating model rather than a parallel process maintained by the risk team. The result should be less friction, clearer ownership, stronger evidence and faster decisions.

Operating across the business is crucial, as significant failures can sit between teams, and begin as small gaps. Such as, a product term not quite matching a system rule, a disclosure trigger not embedded in the workflow or a manual workaround that is undocumented and departs with the employee.

Individually, these gaps may appear minor. But when embedded in high-volume activity, they can scale quickly into widespread customer harm and expensive remediation.

Build what improves decision quality, evidence quality or control reliability. Challenge anything that does not.

Each part of the framework should earn its place.

A proportionate framework should act as a practical operating system for the business. It should help leaders see where risk is building, show where controls may be weakening and direct attention and resources to the areas where they will have the greatest impact.

If you are interested in what a proportionate risk and compliance framework is for your business, just reach out to our team for a chat.

Download ‘Proportionate Risk and Compliance Frameworks’ diagram (PDF)

For many smaller financial institutions, risk and compliance has become increasingly heavy.

New obligations are added, existing frameworks are expanded, and more reports are produced. Management and governance seek more evidence and before long, small teams can feel like they are spending more time maintaining the compliance machine than understanding whether it is actually preventing harm.

A strong risk and compliance framework should help the business see where customer harm, financial stress or control failure is building early enough to act. The goal isn’t to build the largest framework, it’s to build the right framework, with enough rigour to manage the material risks.

Proportionality is sometimes interpreted as a lighter-touch approach. It is better understood as a deliberate choice about where to apply effort. The greater the potential harm, risk or complexity, the stronger the control and assurance should be. Where the risk is lower, there should be room to simplify.

To get here though, you must first understand your obligations. Then a set of questions can ensure on establishing what right-size is for you. A proportionate approach starts with practical questions, such as ‘what harm is this obligation intended to prevent?’, ‘how material is it for our organisation?’ and ‘where are we relying on manual processes, spreadsheets or individual knowledge?’

The answers can then inform the depth of controls needed, the frequency of monitoring and the level of assurance. For example, a high potential harm activity that changes frequently (interest rates or fees for example) may require detailed controls, regular testing and periodic independent assurance. A stable, lower-risk activity may be managed through simpler evidence, periodic sampling and automated reminders.